Why Canadian investors should avoid MLPs

For better or worse, a sizable group of Canadian investors still screens prospective investments by dividend yield. When that search expands beyond Canadian stocks, it often leads into parts of the U.S. market that look attractive on the surface but are poorly understood.

Common examples include American mortgage real estate investment trusts (mREITs) and business development companies (BDCs). Both tend to be highly leveraged and structurally complex, and the headline yield rarely tells the full story. The same applies to Master Limited Partnerships, or MLPs.

What is a master limited partnership?

MLPs occupy the midstream segment of the energy sector. This part of the industry focuses on transporting, storing, and processing oil and gas rather than producing or retailing it. Canadian investors are already familiar with midstream businesses through TSX-listed companies like TC Energy and Enbridge. The difference is that these Canadian firms are conventional corporations, not partnerships.

An MLP is a U.S.-specific pass-through structure designed to generate income from energy-related assets. By operating as a partnership rather than a corporation, an MLP avoids corporate-level tax and distributes most of its cash flow directly to unitholders. That structure is the reason for the eye-catching yields. It is also why MLPs have long been popular with income-focused investors stateside.

The best ETFs in Canada

From a distance, it is easy for Canadians to assume these investments should translate well across the border. Capital markets are similar, the businesses are familiar, and the income looks appealing.

The sticking point is taxation. Differences between Canadian and U.S. tax rules turn MLP ownership into a complicated exercise for Canadian investors, often reducing after-tax returns and creating ongoing administrative headaches. Those frictions matter more than most investors realize.

Here is what Canadian investors need to know about U.S. MLPs, why they are usually best avoided, and which alternatives offer exposure to similar businesses without the same tax complications.

The tax headaches of MLPs for Canadian investors

For Canadian investors, the problems with U.S. master limited partnerships come down to two main issues: withholding tax and reporting requirements.

Most Canadians are already familiar with how U.S. withholding works. When you own U.S.-domiciled stocks or exchange traded funds (ETFs), 15% of dividends are typically withheld at source. That withholding can be avoided by holding those securities inside a Registered Retirement Savings Plan (RRSP), thanks to the Canada-U.S. tax treaty.

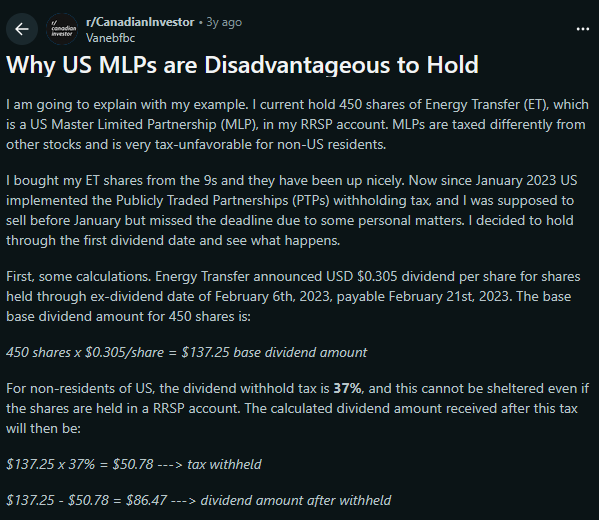

MLPs are treated very differently. They do not benefit from that treaty treatment. Distributions from MLPs are fully subject to U.S. withholding tax. Worse, the rate is not 15%. It is up to 37%. This withholding applies even inside registered accounts, including RRSPs.

Source: r/CanadianInvestor

That means more than one third of each distribution can disappear before it ever reaches your account. This is especially damaging because most of the long-term return from MLPs comes from reinvested distributions rather than price appreciation.

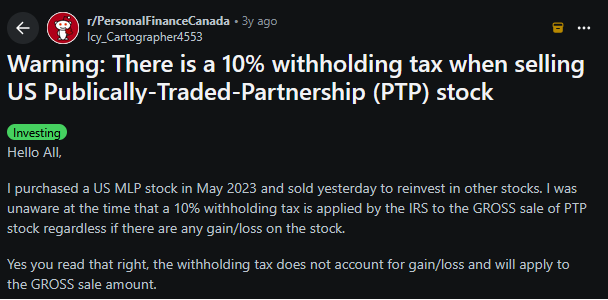

It does not stop there. When you sell an MLP, there is an additional 10% withholding tax applied to the gross proceeds by the Internal Revenue Service (IRS), because MLPs are classified as publicly traded partnerships. This is not a capital gains tax. It is withheld regardless of whether you are selling at a gain or a loss.

There are numerous real-world examples of Canadian investors discovering this the hard way. Some have bought and sold the same MLP multiple times, only to find that 10% was withheld on each transaction.

Source: r/PersonalFinanceCanada

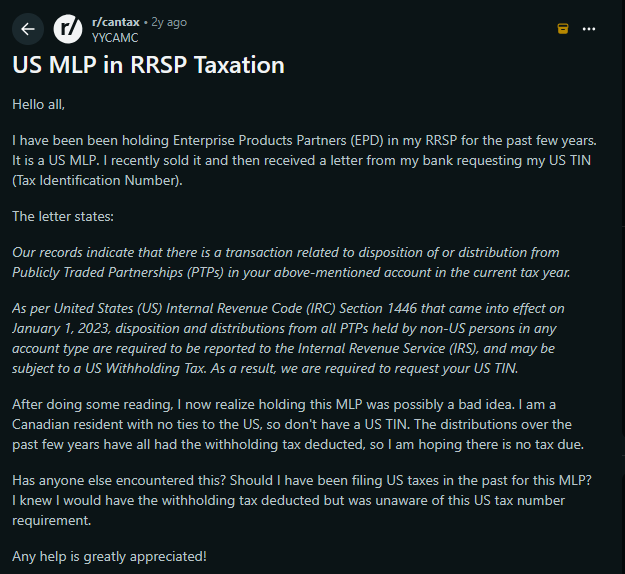

The final complication is tax reporting requirements. When you own a typical U.S. stock, you receive a 1099-DIV form that summarizes your income. With an MLP, you are not a shareholder. You are a partner. That means you receive a Schedule K-1.

A K-1 reports your share of the partnership’s income, deductions, and credits. It is far more complex than a standard dividend slip, and it creates a U.S. tax filing obligation. In theory, you are required to file a U.S. tax return to properly report this income to the IRS.

Source: r/cantax

Some investors choose to ignore this requirement, but that is a risky approach. Dealing with cross-border tax issues after the fact is rarely worth the trouble.

Taken together, these issues are hard to overlook. High withholding taxes on distributions, mandatory withholding on sales, and ongoing U.S. tax reporting obligations all apply even in registered accounts. For those reasons alone, I personally believe U.S. MLPs are generally a poor fit for Canadian investors, no matter how attractive the headline yield may look.

Canada’s best dividend stocks

MLP alternatives for Canadian investors

The simplest alternative is also the most obvious one. You can target the same part of the energy industry, the midstream segment, without using MLPs at all. That means sticking with regular corporations, and the TSX offers plenty of options.

Companies such as Enbridge, TC Energy, and Pembina Pipeline all operate fee-based energy infrastructure with long-term contracts tied to oil and gas volumes. These businesses are similar to U.S. MLPs at the asset level. The difference is how they are taxed.

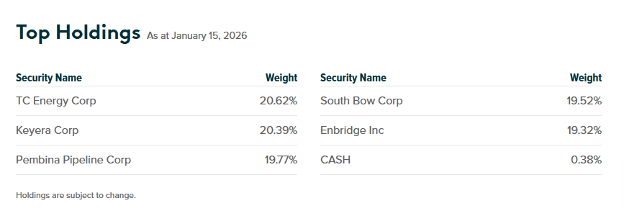

These companies pay eligible dividends, which qualify for the dividend tax credit in taxable accounts. You avoid foreign withholding issues, avoid U.S. tax filings, and still receive above-average yields from essential infrastructure assets. You can even buy a basket of them via an ETF like the Global X Equal Weight Canadian Pipelines Index ETF (PPLN).

Source: Global X Canada

However, if you still want exposure to MLPs specifically, you can use a U.S.-listed ETF. There are two possibilities within this niche, each with their own trade-offs.

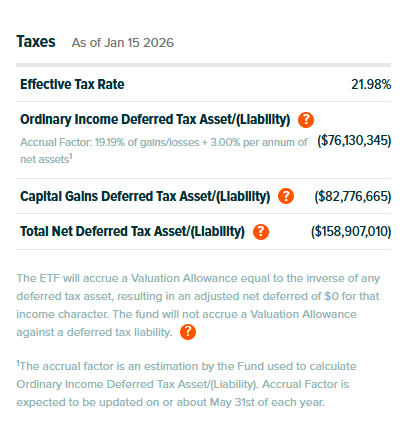

The first approach is a pure-play MLP ETF that is structured as a corporation. These funds own only MLPs but are taxed at the corporate level. The distributions they pay often retain MLP characteristics, including a large return of capital component, but there is an important trade-off. Because the ETF itself is a corporation, it accrues deferred income-tax liabilities. These reflect depreciation from the underlying MLPs and unrealized capital gains in the portfolio. The amount depends on the U.S. federal corporate tax rate and applicable state taxes.

This deferred tax liability can act as both a headwind and a tailwind. It may dampen gains during strong markets and soften losses during downturns. Over long periods, however, the practical effect has often been a significant tracking error.

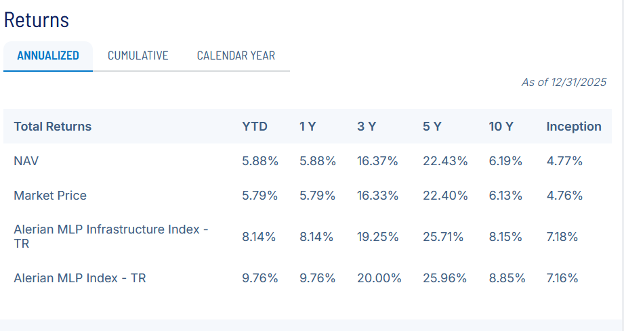

A commonly cited example is the Alerian MLP ETF (AMLP). Over the past decade, its net asset value return has trailed its benchmark index by a wide margin. A large part of that gap comes from deferred taxes, along with its relatively high 0.85% expense ratio.

Source: ALPS Funds

Lower-cost options do exist. The Global X MLP ETF (MLPA) charges about 0.45% and pays a decent 7.94% 30-day SEC yield (a standardized calculation for funds developed by the U.S. Securities and Exchange Commission), but it still carries the same deferred tax mechanics. Global X even discloses the fund’s effective tax rate on its website, which highlights how meaningful this drag can be.

Source: Global X

There is another structure that avoids this issue, with a different compromise. U.S. ETFs that limit MLP exposure to 25% or less can be structured as registered investment companies (RICs) under the Investment Company Act of 1940. These are pass-through vehicles that do not pay corporate tax, as long as they distribute income and realized gains.

The trade-off is that you no longer get pure MLP exposure. The remaining holdings are typically incorporated midstream companies. These often include U.S.-listed shares of familiar names like ONEOK, Kinder Morgan, and Williams Companies, along with U.S. listings of Canadian firms.

An example is the Global X MLP & Energy Infrastructure ETF (MLPX). It carries the same 0.45% expense ratio as its pure-play sibling, but its yield is lower at 5.12% on a 30-day SEC basis because it is not fully invested in MLPs. The benefit is simpler taxation and no deferred tax liability dragging on returns.

Taxes are inevitable, so at least keep it simple

Whichever ETF structure you choose, there are two clear advantages compared with owning MLPs directly. Both types of ETFs issue 1099-DIV forms rather than Schedule K-1s, and they eliminate the 37% withholding on distributions and the 10% withholding on sales. You simply deal with the usual 15% foreign withholding tax on dividends, which you can avoid by putting them in a RRSP.

For Canadian investors who insist on MLP exposure, ETFs are the least painful route. For most others, Canadian and U.S. midstream corporations can offer similar economics with far fewer tax complications.

Get free MoneySense financial tips, news & advice in your inbox.

Read more about investing strategies:

- The best GIC rates in Canada for 2025

- If not bonds, then what?

- Can you hedge against a market crash with ETFs?

- Is Wealthsimple’s new Physical Gold Trading worth it?

The post Why Canadian investors should avoid MLPs appeared first on MoneySense.

You May Also Like

Wormhole launches reserve tying protocol revenue to token

Kalshi debuts ecosystem hub with Solana and Base